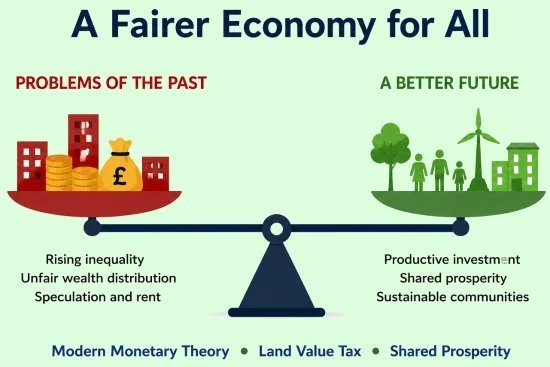

Neoliberal Economics, MMT and LVT

For more than forty years, economic policy in many developed countries has been dominated by neoliberal thinking. Lower taxes, deregulation, privatisation and reduced government intervention have been promoted as the best way to create prosperity. While this approach has undoubtedly encouraged innovation and increased global trade, it has also produced some unintended consequences. Perhaps the most significant has been a widening gap between rich and poor, driven largely by rising asset values rather than increases in productive economic activity.

Modern Monetary Theory (MMT) offers a radically different view of how governments should manage their economies. Rather than treating government spending as something that must be funded primarily through taxation or borrowing, MMT argues that sovereign governments issuing their own currency can create money as required. The real limitation is not money itself but inflation. This shifts the debate from "How can government afford to spend?" to "How can government spend enough to achieve full employment without creating excessive inflation?"

The contrast between these two approaches highlights one of the biggest challenges facing modern economies: how to encourage growth while ensuring that prosperity is shared more fairly.

Neoliberal economics assumes that reducing taxes on wealth and business encourages investment, with benefits eventually "trickling down" throughout society. In practice, much of the additional wealth has accumulated in land, property and financial assets. Rising house prices, increasing land values and booming stock markets have benefited those who already owned substantial assets, while younger generations and lower-income households have found it increasingly difficult to accumulate wealth.

This concentration of wealth has several damaging effects. High property prices increase the cost of living, discourage productive investment and transfer increasing amounts of national income into rents and mortgage payments. Landowners often benefit from increases in land value created not by their own efforts but by public investment, population growth and planning decisions. A new railway station, school or business park can dramatically increase surrounding land values, yet these gains accrue almost entirely to private owners.

Please click the image below for a larger version.

MMT begins from a different premise. It argues that unemployment represents evidence that government spending is too low relative to the productive capacity of the economy. Rather than accepting unemployment as inevitable, governments should spend sufficiently to ensure that everyone willing to work can find employment. Such spending could finance infrastructure, scientific research, healthcare, education, environmental restoration and many other activities that improve national productivity.

Critics often argue that this would simply create inflation by printing money. MMT acknowledges this risk but argues that inflation - not government debt - is the true constraint on public spending. When an economy approaches full productive capacity, additional spending must be balanced by measures that reduce excess demand.

Traditionally, governments have relied upon higher interest rates to control inflation. Central banks increase borrowing costs, making mortgages, business investment and consumer loans more expensive. This reduces spending across the economy.

However, interest rate policy has significant drawbacks. It affects borrowers far more than wealthy asset owners. Young families with mortgages, businesses investing for growth and first-time buyers bear the burden, while individuals with large property portfolios or substantial savings may be relatively unaffected or may even benefit from higher interest income. The result is that one of the principal tools used to control inflation often increases wealth inequality.

A Land Value Tax (LVT) offers an alternative that aligns remarkably well with the principles of MMT.

Unlike taxes on income, profits or productive investment, a Land Value Tax falls only on the unimproved value of land. Buildings, machinery and business activity are not taxed. The tax captures part of the economic value created by society rather than by the landowner. Since the quantity of land is fixed, an LVT cannot discourage its production or drive investment overseas. Economists across the political spectrum have long recognised that it is among the least economically distortive forms of taxation.

Within an MMT framework, LVT could become one of the principal mechanisms for controlling inflation. As government spending stimulates economic activity, infrastructure improvements and stronger demand often increase land values. Rather than allowing these gains to accumulate entirely as private windfall profits, higher land values would automatically generate higher tax revenues. This withdraws purchasing power from the economy precisely where much of the inflationary pressure is emerging.

The distributional effects are equally important. Today, much of the wealth created by economic growth is reflected in rising land prices. Those who already own valuable land become wealthier without necessarily contributing additional productive effort. An effective Land Value Tax recycles part of these unearned gains back into public finances, allowing governments to reduce taxes on labour, enterprise and productive investment.

This changes economic incentives. Instead of rewarding speculation in land, the tax encourages owners to develop land efficiently or release it to those who will. Vacant sites become less attractive to hold indefinitely in anticipation of future price rises. Urban regeneration becomes easier, housing supply can increase and land prices may become more stable over the long term.

Government spending financed under MMT could therefore focus on investments that raise national productivity while the accompanying Land Value Tax moderates inflationary pressures and redistributes part of the resulting wealth. Infrastructure projects, education, healthcare and scientific innovation all increase the productive capacity of the economy. As these investments enhance surrounding land values, part of that publicly created wealth is automatically returned to the public purse.

No economic system is perfect. Neoliberal policies have delivered greater efficiency in many sectors but have also contributed to rising inequality and an over-reliance on asset appreciation as the primary source of wealth. MMT offers a more active role for government but requires credible mechanisms to prevent inflation and maintain confidence in the currency.

A well-designed Land Value Tax could provide one of those mechanisms. By taxing economic rent rather than productive effort, it simultaneously discourages speculation, moderates inflationary pressures, captures publicly created land value and supports a fairer distribution of wealth. In combination with carefully targeted government investment, it offers a coherent framework for achieving both sustained economic growth and greater economic fairness - an outcome that neither traditional neoliberalism nor conventional monetary policy has consistently succeeded in delivering.